Benedictory Address by Shri Kanchi Kamakoti Peetadhipati Jagadguru Pujyashri Shankara Vijayendra Saraswati Shankaracharya Swamiji

On July 06, 2026, India Foundation in collaboration with India Habitat Centre, New Delhi, organised a Benedictory Address that was delivered by Shri Kanchi Kamakoti Peetadhipati Jagadguru Pujyashri Shankara Vijayendra Saraswati Shankaracharya Swamiji. The profoundly spiritual and intellectually enriching benedictory address was organised in the Stein Auditorium, India Habitat Centre in New Delhi. The prestigious session was presided over by the Hon’ble Lieutenant Governor of Delhi, Sardar Taranjit Singh Sandhu. The session was attended by more than 400 participants comprising policymakers, diplomats, and scholars.

Setting a highly reverent tone for the evening, Lieutenant Governor Sardar Taranjit Singh Sandhu delivered the inaugural welcome address. He extended a warm and respectful welcome to Shankaracharya Swamiji on behalf of everyone present, emphasizing that the occasion served as a vital bridge connecting the national capital with one of India’s oldest living spiritual traditions, which represents an unbroken civilizational legacy spanning over 2,500 years. The Lieutenant Governor lauded Swamiji, noting that he accepted the path of sanyas at the age of thirteen and has since devoted more than four decades to spiritual guidance, public service, and nation-building. He also specifically mentioned the numerous Vijaya Yatras carried out by Swamiji in different parts of the country, especially North East, Jammu and Kashmir, and Punjab, and their role in national integration and social cohesion.

Jagadguru Pujyashri Shankara Vijayendra Saraswati Shankaracharya Swamiji delivered his highly anticipated benedictory address. He said that the main purpose of his visit to Delhi was to attend the Kumbhabhishekam of the Devi Kamakshi temple near Jawaharlal Nehru University and a religious function in the name of Lord Murugan. Swamiji went on to explain the great legacy of his Paramacharya, who lived for a hundred years and gave strong spiritual and moral support to India’s freedom struggle, and he also mentioned the historic meeting in Kerala in 1927, when the Paramacharya met Mahatma Gandhi and C. Rajagopalachari and blessed and encouraged the independence movement. He also highlighted the Paramacharya’s unwavering commitment to the Swadeshi spirit, and how in 1922, after a bath at Dhanushkodi, the Paramacharya renounced traditional silk clothes and chose to wear only saffron-dyed khadi for the rest of his life.

In his benedictory address, Shankaracharya Swamiji also referred to the Kanchi Peeth’s close relationship with the youth of the country and its governing institutions, and how the Peeth had played a very important role in the post-1947 era, particularly in the framing of the Constitution. He narrated the story how the clauses in Articles 25 and 26 in the constitution were drafted with the help of scholars from Kanchi Peeth after dialogue with constitutional stalwarts like Dr B R Ambedkar and Sardar Vallabhbhai Patel, so that India’s ancient cultural and religious institutions could continue to thrive with dignity and autonomy in the new democratic framework.

Underlining the importance of preserving India’s civilisational memory, the Shankaracharya Swamiji elaborated on the work the Kanchi Peeth had undertaken in the areas of traditional knowledge and epigraphy, and he recalled how the recitation of the Atharva Veda had once almost disappeared and was confined to the Pancholi family in Gujarat. The Peeth had deputed scholars to Gujarat for several years to study and preserve the oral tradition, and this work had resulted in over 200 Atharva Veda scholars today. The Swamiji also mentioned the establishment of the Uttankita Vidyaranya Trust to translate and publish ancient Sanskrit inscriptions from India and abroad. , and he mentioned a key publication on a 1,400-year-old inscription from ancient Gandhara (in present-day Afghanistan) which recorded the consecration of a Ganesha temple around 600 AD. Such evidence, he said, was proof of India’s deep and extensive cultural presence in Asia, therefore, it highlighted the significance of the Peeth’s efforts in preserving the country’s cultural heritage.

The Shankaracharya Swamiji also shed light on the Kanchi Peeth’s socio-economic programmes and initiatives, particularly those spearheaded by his immediate predecessor, Sri Jayendra Saraswati, and he said that in the 1980s, the institution was giving much thrust to inclusive growth through grassroots programmes like loan melas and support to small and micro-industries, similar to the present-day Vishwakarma Yojana, as well as large-scale temple renovation activities. Shankaracharya Swamiji said that democracy must not be viewed as a Western concept only because, citing the example of King Dasharatha, who sought the views and approval of his people before deciding to crown Lord Rama, he showed that democratic consultation and respect for public opinion have been an integral part of India’s civilisational tradition from ancient times.

Shankaracharya Swamiji painted a powerful vision of the future of the nation as he spoke of a Triveni of ‘Trade, Tradition and Technology’, in which India’s development model would focus on converting villages into specialist service and economic zones that were closely linked to urban resources, so that rural communities could flourish without being forced into migration. Shankaracharya Swamiji said he had no hesitation in accepting scientific and technological advancements from abroad, but he said India did not need foreign advice or guidance on matters of culture, human rights and civilisation, because these values were well-entrenched in India’s own ancient traditions. Shankaracharya Swamiji ended his benedictory address with a special emphasis on youth and women, and he announced the revival of the Yuva Tirth Yatri Sangh for the youth of Delhi, which would help to connect young graduates with ancient pilgrimage centres and strengthen their civilizational identity; therefore, he also called for the practice of “Laghu Nyas”, or micro-charity, among women, as a means of promoting cultural values at the grassroots level. Swamiji closed the function with prayers to Lord Chandramouleeshwara and Goddess Kamakshi, wishing the people of Delhi and the nation peace, prosperity and harmony.

13th edition of Katha

India Foundation organised the 13th edition of Katha, its storytelling session series, on the theme ‘German Folklore, Fairy Tales, and Living Traditions’, at Gulmohar Hall, India Habitat Centre, New Delhi, on 30 June 2026. The session featured Ms. Judith Weinberger-Singh, Resident Representative, Hanns Seidel Foundation India, as the lead storyteller speaker. It was chaired by Dr. Ram Madhav, President, India Foundation, and moderated by Mr. Apurv Mishra, Consultant, Economic Advisory Council to the Prime Minister. Now grown well beyond its original circle of regular attendees, the gathering retained the informal character of a club rather than a seminar, with listeners invited to sketch the tales they heard as an active part of the storytelling tradition.

Opening the session, the chair reflected on a recurring insight from the series: that at the level of mythology and folklore, striking similarities surface across peoples, with shared themes, spirit, and moral messages transcending geographical and national boundaries. He noted that although Germany is a relatively young nation-state unified in the nineteenth century, it draws on a far older cultural inheritance, and that many stories widely assumed to be American are in fact German in origin.

Ms. Weinberger-Singh structured her talk around the forest of her native Bavaria before turning to the more familiar Grimm tradition. She introduced two lesser-known regional customs: Wolfauslassen, the “letting out of the wolves,” in which herdsmen mark the end of the grazing season and the onset of winter through processions of bells and poetry, a ritual dating to the seventeenth century and still practised in her district; and the Rauhnächte, the twelve nights between Christmas and Epiphany, when the boundary between the human and spirit worlds is believed to thin, giving rise to the Wild Hunt of ghosts and witches and to customs of incensing the home and avoiding hung laundry.

Turning to the Brothers Grimm, she explained how their collection of oral folklore in the early nineteenth century was bound up with German nation-building and linguistic identity at a time when French still dominated intellectual life. She contrasted two tales: Aschenputtel, the darker original of Cinderella first written down in 1812, in which virtue, piety, and hard work are ultimately rewarded; and Puss in Boots, a tale of French origin excluded from the definitive 1857 collection, in which cunning rather than virtue drives success, and at a moral cost. She closed by asking whether one can truly be the architect of one’s own destiny, and by what values such a pursuit should be guided.

In his concluding remarks, the chair drew a parallel with the Panchatantra and its animal fables, observing that storytelling across cultures encodes moral instruction beneath even seemingly irrational surfaces. Closing the session, the moderator drew out a thread from the talk: that the Grimms, like the compilers of the Panchatantra, the Arabian Nights, and Perrault’s tales, were not authors but custodians of an oral tradition rooted in the voice of ordinary people, a reminder of folklore’s shared human wellspring.

July-August 2026: India Foundation Journal

Anchoring the Indo-Pacific: Geopolitical Strategic Balancing and Supply Chain Resilience in India-Vietnam Ties

Introduction

The India-Vietnam Enhanced Comprehensive Strategic Partnership (ECSP), upgraded in May 2026, is grounded in shared geopolitical concerns and economic complementarities. The upgrade significantly deepens cooperation across defence, supply chain diversification, critical minerals, and financial and digital connectivity. It also aligns India’s “Act East Policy” and “Developed India @2047” with Vietnam’s “Vision of a developed country by 2045”.

Against this backdrop, the Paper argues that to understand why these two middle powers are deepening their alliances, it is important to study the geopolitical alignments, defence convergences, and economic complementarities between India and Vietnam. Given the changing power dynamics in the Indo-Pacific, the Paper also argues how Vietnam fits into this broader geopolitical balance.

To analyse the argument, the Paper draws on major international relations theories, including ‘Neorealism’, ‘Liberal Institutionalism’ and ‘Constructivism’, and reflects on why and how India and Vietnam are deepening their ties. It also examines the evolution of India-Vietnam relations and the recent upgrade to ECSP. Geopolitical balancing by both countries amid the shift in power in the Indo-Pacific is also highlighted. The Paper further explores key drivers of growth in sectors such as manufacturing, supply chains, critical minerals, human resource mobility and EV manufacturing. Finally, the Paper focuses on the immense potential of tourism and people-to-people exchanges to foster a comprehensive political and economic relationship between the two countries.

Theoretical Framework

Analysing the India-Vietnam Enhanced Comprehensive Strategic Partnership (ECSP), which encompasses robust India-Vietnam relations and critical supply-chain frameworks, requires a multidimensional approach. The Paper uses an international relations theoretical framework to analyse this partnership. The evolution of these multifaceted relations can be evaluated through the lenses of three core international theories: Neorealism, Liberal Institutionalism and Constructivism.

Neorealism highlights the anarchic nature of the international system, in which states seek to maximise security by balancing against rising threats. The primary factors shaping states’ behaviour are the distribution of power and the need to balance against potential hegemonies. From a Neorealist perspective, the India-Vietnam partnership exemplifies external balancing, particularly in response to China’s territorial claims in the South China Sea and its growing assertiveness in the Indo-Pacific. Both countries are prioritising independent foreign policies while strengthening their defence capabilities. Vietnam seeks to enhance its strategic presence by diversifying its diplomatic options through partnerships with a rising Asian power, such as India. By contrast, India uses its deepening defence and maritime ties with Vietnam as a geostrategic lever to project power in response to the rise of an assertive China and the shifting balance of power in the Indo-Pacific.

Liberal Institutionalism holds that even in an anarchic system, absolute gains can be achieved by strengthening institutional engagement. According to this view, states cooperate out of mutual self-interest, facilitated by international regimes, institutions, and economic interdependence. The liberal institutional perspective views ECSP through the lens of institutional networks and economic interdependence. Both nations are concerned not only with security balancing but also with institutional integration and economic partnerships. Bilateral agreements to raise the trade target to USD 25 billion by 2030, digital payment linkages between their central banks, and cooperation on critical rare-earth minerals have highlighted their joint efforts to build resilient supply chains. Institutional collaborations through the Indo-Pacific Oceans Initiative (IPOI) emphasise a shared security architecture, ‘freedom of navigation’, and a ‘rules-based order’ in the South China Sea. These frameworks reduce transaction costs and build long-term trust, making both economies mutually resilient to external threats.

Constructivism emphasises the role of shared ideas, norms, identities, and socialisation in shaping state behaviour. It holds that national interests are not fixed by material power alone but are socially constructed through interaction. According to Constructivism, shared history, civilisational linkages, and anti-colonial solidarity construct a powerful narrative of mutual trust and partnership. India’s ‘Act East’ policy and Vietnam’s integration into the IPOI provide the ideological and normative backbone of their alignment. Both nations share a post-colonial identity as rapidly growing, aspirational societies with complementary national visions – India’s ‘Viksit Bharat 2047’ and Vietnam’s ‘2045 Development Vision’. Their shared commitment to strategic autonomy and to the United Nations Convention on the Law of the Sea (UNCLOS) provides a strong normative foundation for cooperation. Taken together, these factors turn a strategic and security pact, amid fluctuating geopolitical pressures, into a socially constructed partnership.

Evolution of India-Vietnam Relations

The historical connections between India and Vietnam have enriched our ancient literature and mythology. Originating in the 2nd century BCE, these linkages through trade and commerce can be traced back to the establishment of the Champa Kingdom, which flourished in what is now central and southern Vietnam. As a pivotal maritime centre, it has fundamentally shaped the region’s geopolitical landscape in ancient times. Historically, it has played a significant role in shaping the culture, commerce and connectivity between India and Vietnam[1]. It has served as a vital bridge for the transmission of Indian social, political and cultural traditions to Southeast Asia and for forging lasting links with the Indian subcontinent.

These centuries-old ties continue to shape contemporary bilateral relations, forming a civilisational foundation for the strategic partnership between India and Vietnam today. The Hindu Kingdom of Champa and Indian Buddhist philosophy and religion also blended seamlessly with Vietnam’s indigenous belief system. India also provided “crucial moral and political support to Vietnam during its national liberation struggle against France and the United States”.[2]

The foundation of the friendship was laid by India’s first Prime Minister, Jawaharlal Nehru, and Vietnam’s President Ho Chi Minh. As a visionary leader, Ho Chi Minh fought American troops with an unyielding spirit and became a household name in Kolkata, India, through the slogan “Mera Naam Tera Naam, Vietnam–Vietnam” (“My name and your name are the same as Vietnam”), which proclaimed solidarity with the people of Vietnam in their fight against American imperialism[3].

The bilateral ties were upgraded to ‘Strategic Partnership’ in 2007 and to ‘Comprehensive Strategic Partnership’ (CSP) in 2016[4]. A decade of this CSP (2016-26) and 54 years of diplomatic ties (1972-2026) have resulted in the elevation of ties to the‘Enhanced Comprehensive Strategic Partnership’ (ECSP) in 2026.

India and Vietnam have been reported as among the fastest-growing economies in the world. Both countries have achieved sustained economic growth and trade diversification over the past three decades. Vietnam’s ‘Doi Moi’ reforms of the late 1980s and India’s ‘New Economic Policy’ of 1991, both focused on liberalisation, privatisation and globalisation, mark parallel growth trajectories for both countries. Together, the two countries have pursued market-led, export-oriented growth strategies and sought to deepen their integration into regional and global value chains. Given their political histories of reform and complementarities, they have emerged as globally integrated, dynamic economies in the region.

In foreign policy and diplomacy, both India and Vietnam have recast their strategies since the late twentieth century. Economic reforms have led to diversification and greater multilateral engagement in Vietnam. India’s diplomacy in the post-Cold War era has evolved from classical non-alignment to multi-alignment, emphasising strategic autonomy within a rules-based order. Both countries have converged on a strategic outlook of multipolarity and diversified partnerships in a complex, interdependent world.

As two growing economies of the Global South, India and Vietnam have emphasised the importance of addressing shared challenges related to international law and of ensuring the voices and rights of developing countries. Leaders of both countries have also agreed to work closely on regional and international platforms to ‘promote peace, stability, and development’.

During his recent visit, President To Lam called India a “centre of growth and innovation in the world” and discussed linking the “strategic visions and development strategies of both countries to better address the turmoil in the situation of the world today”[5]. As both countries move towards the goal of becoming‘developed countries’ – Vietnam by 2045 and India by 2047 – they share a vision for growth and mutual prosperity. It is fitting to quote Prime Minister Modi’s words, “Together, we will walk, grow, and win”, which reflect the foundational vision for collective development[6].

Towards Enhanced Comprehensive Strategic Partnership

India and Vietnam officially elevated their bilateral relations to an ‘Enhanced Comprehensive Strategic Partnership’ (ECSP) during the State visit of the Vietnamese President, H. E. To Lam to India[7]. The upgrade marks the 10th anniversary of the ‘Comprehensive Strategic Partnership’ signed in 2016, deepening their bilateral cooperation. Both countries have institutionalised a multifaceted partnership in the region, anchored in defence and security cooperation, economic and green transformation, and strategic and regional alignment.

For India, Vietnam is an important factor in its ‘Act-East Policy’ and a significant partner in the ‘Vision MAHASAGAR’. As part of ECSP, Vietnam has announced its intention to join India’s ‘Indo-Pacific Ocean Initiative’ (IPOI). This integration of Vietnam into IPOI will be a strategic milestone for expanding India’s footprint in the regional architecture and enabling Vietnam to pursue geopolitical balancing.

Altogether, India and Vietnam concluded thirteen agreements during the May 2026 visit to India by the President of Vietnam, H. E. To Lam. The agreements cover a wide range of issues, including defence and maritime security; culture and tourism; critical minerals and digital technology; health and pharmaceuticals; trade, commerce and investment; and urban management and development partnership[8].

Both nations aim to reach USD 25 billion in bilateral trade by 2030, with two-way trade currently at around USD 16 billion[9]. While traditional items still dominate the trade basket between India and Vietnam, investments in new technology sectors, including the digital economy, technology and innovation, critical minerals, renewable and green energy, semiconductors, pharmaceuticals, healthcare, space technology, cybersecurity, the blue economy and marine technology, are increasingly significant drivers of bilateral trade growth between India and Vietnam.

Enhanced engagement in both “traditional and emerging areas of defence cooperation and defence systems procurement” between India and Vietnam has been the primary focus of the joint statement issued by the two leaders[10]. Collaboration in “oceanography, including areas such as ocean observing platforms, data management, ocean prediction and services, capacity building and maritime scientific research” has also been emphasised[11].

Digital technologies and critical emerging technologies have also been key themes in the joint statement between the two countries. It focuses on “facilitating greater collaboration and partnership in critical and emerging technology areas such as Digital Public Infrastructure, 6G, Artificial Intelligence, space and nuclear technology, marine sciences, biotechnology, pharmaceuticals, advanced materials and critical minerals. Cooperation will focus on practical initiatives such as joint research, R&D centres, and product development as mutually beneficial.”[12] Under this initiative, “the Reserve Bank of India and State Bank of Vietnam” have agreed to promote financial innovation and digital payments. They have decided to link their respective platforms via QR codes for retail payments to facilitate tourism and business on both sides.

India and Vietnam are deepening bilateral healthcare ties to modernise medical infrastructure. The cooperative framework between the two countries covers digital health transformation, the integration of Artificial Intelligence into medicine, and expanded research into traditional medicine. Both countries have signed a tourism cooperation memorandum and agreed to “promote sustainable two-way tourism, including cultural and heritage, medical and wellness tourism”.[13] They have also committed to strengthening air connectivity and logistics cooperation by expanding direct flights.

To establish institutional linkages and a formal framework enabling India and Vietnam’s largest megacities to collaborate, “a memorandum for the establishment of friendship and cooperation between the Brihanmumbai Municipal Corporation (BMC) in Mumbai and the Ho Chi Minh City People’s Committee in Vietnam has been signed.”[14] As a key pillar of bilateral cooperation and the deepening of people-to-people ties, the joint statement focuses on “greater student, faculty and research exchanges between universities and think tanks of the two countries”. The two countries have also signed a memorandum on “documentation, conservation, digitisation and online dissemination of Cham manuscripts of Indian origin currently preserved in Vietnam”.

India-Vietnam Strategic Balancing

India and Vietnam have officially elevated their bilateral ties to an ‘Enhanced Comprehensive Strategic Partnership’ (ECSP). A core element of this upgraded framework is geostrategic balancing against China’s growing assertiveness in the South China Sea. This aligns with the combination of Vietnam’s maritime frontline position and India’s ‘Act East policy’ and broader Indo-Pacific ambitions.

Vietnam shares a sensitive land border with China and faces complex maritime disputes. It balances these pressures by cultivating deep defence and political ties with major powers. In this endeavour, India is a crucial partner for Vietnam in maintaining its strategic autonomy. For India, a strong Vietnam is a friendly partner in the Indo-Pacific, preventing unilateral domination in Southeast Asia and securing vital sea lanes of communication through which a significant share of India’s global trade flows.

Both nations advocate a ‘free, open, and rules-based’ Indo-Pacific, with strict adherence to the ‘United Nations Convention on the Law of the Sea’ (UNCLOS) and to freedom of navigation. Vietnam has joined India’s ‘Indo-Pacific Oceans Initiative’ (IPOI). This alignment reflects strategic convergence and enables close cooperation with India’s regional maritime architecture without directly forming a formal anti-China alliance.

Defence remains the cornerstone of the partnership between India and Vietnam. The two nations have established a new 2+2 Strategic Defence Dialogue and are focusing on naval interoperability, port calls, defence equipment procurement, capacity building and technology co-production. Both countries are working to enhance defence procurement. This includes advanced negotiations for Indian military exports to Vietnam, such as the BrahMos supersonic cruise missile, which Vietnam seeks to strengthen its coastal defence posture in the South China Sea.

Amid reports that Vietnam is finalising a BrahMos deal with India, a significant shift is underway in the region’s geopolitics. Although Vietnam maintains strong economic relations with China, it has increasingly sought to diversify its defence and strategic partnerships with India. Vietnam’s defence preparedness reflects China’s growing monopoly and hegemonic designs in the South China Sea and its maritime expansion, leading to a changing balance of power in the region. Furthermore, by expanding its BrahMos deal in Southeast Asia (Vietnam being the third country after the Philippines and Indonesia), India is increasing its influence and emerging as a ‘net security provider’, countering China’s hegemony in the region.

Key Economic Drivers and Sector Goals

India and Vietnam are accelerating economic integration under their ‘Enhanced Comprehensive Strategic Partnership’, aiming to “expand the bilateral trade target to USD 25 billion by 2030”. Beyond defence, the two nations aim to build resilient supply chains, enhance bilateral investment, and strengthen cooperation in the digital economy.

Manufacturing & Supply Chains: India and Vietnam are rapidly integrating their manufacturing and supply chains to form a powerful regional “China-Plus-One” alternative. The two manufacturing ecosystems are highly complementary rather than competitive. India, supported by large government programmes such as the Production Linked Incentive (PLI) Scheme, is attracting significant global investment in electronics, pharmaceuticals, and automotive manufacturing. Vietnam is actively diversifying its manufacturing sources and increasing imports of industrial inputs (such as iron, steel, and auto parts) from India to support its export needs. India also hopes to benefit from Vietnam’s highly efficient export processing zones to boost its own “Make in India” initiatives. Both nations are positioning themselves as complementary hubs for American and European businesses restructuring their global supply chains away from China.

Rare Earth and Critical Minerals: India and Vietnam are focusing on rare earths and critical minerals to secure supply chains and reduce reliance on monopolistic markets. This partnership combines Vietnam’s vast rare earth reserves with India’s surging demand and expanding processing capabilities. “Through new initiatives in critical minerals, rare earths, and energy cooperation, we will ensure the economic security and supply chain resilience of both sides.”[15]

The Government of Vietnam has identified “the mining industry, including the rare earth minerals sector, as a priority for development, and has introduced measures to attract foreign investment, such as tax incentives, streamlined procedures for obtaining mining licences, and the establishment of industrial zones dedicated to mining and processing.” The strategic partnership between India and Vietnam on rare-earth elements makes Vietnam a crucial partner for India’s growing industrial and green technology needs. Rare-earth elements are also crucial for achieving “self-reliance and long-term security of the country, as the manufacturing of products across industries such as defence, aerospace, electronics, electrical equipment, including renewable energy, is highly dependent on the rare earth elements.”[16]

Healthcare & Pharmaceuticals: The India-Vietnam healthcare and pharmaceutical partnership is rapidly expanding, driven by India’s position as a global supplier of generic medicines and Vietnam’s growing domestic pharma market. In light of this, Vietnam aims to increase its reliance on Indian companies for cost-effective medicines and drug procurement for its public hospitals. This reflects Vietnam’s commitment to move away from its historical reliance on a single source of supply, cementing India as its most trusted and cost-effective partner for pharmaceuticals and medical equipment. They are also collaborating on traditional medicine, digital healthcare transformation, and AI applications in the health sector.

Human Resource Mobility: India and Vietnam are rapidly deepening their bilateral relationship, with a major focus on human resource mobility and capacity building. As part of the ECSP, both countries view workforce development and human resource mobility as crucial to securing supply chains, driving economic growth, and achieving strategic autonomy in the region. India is one of the largest global exporters of healthcare professionals, including doctors and nurses, as well as highly skilled corporate employees, IT specialists, and technical advisors. Both countries have prioritised knowledge sharing and the integration of startup ecosystems by building corporate networks. In the evolving technology landscape, India’s experienced IT professionals are migrating to and partnering with Vietnam, as the country develops its digital economy and semiconductor industries. We find Indian expatriates frequently working in Vietnam as managers, tech experts, and executives in sectors such as manufacturing, renewable energy, and software.

India’s Consumer Market & The EV Boom: India’s rapidly growing consumer market is highly attractive to Vietnamese companies, particularly in the electric vehicle (EV) sector. Vietnamese EV giant VinFast views India’s market as a major priority, given the local appetite for sustainable and affordable mobility. VinFast is investing USD 500 million to build a large, integrated EV manufacturing plant in Thoothukudi, Tamil Nadu. The facility, which can scale to 150,000 vehicles annually, will allow VinFast to leverage the government’s EV manufacturing ecosystem. It has been reported that “VinFast also plans to establish a nationwide dealer network to build the brand with the commitment of good cars, good prices and excellent after-sales services.”[17] It is also launching a “green and eco-friendly” taxi service in the Delhi-NCR region and expanding its operations to Bengaluru and Hyderabad by the end of 2026[18].

Strengthening People-to-People Exchanges

Cultural and people-to-people ties provide the foundation on which the political and economic partnership thrives. In this regard, India and Vietnam have focused on tourism as a vital pillar of economic growth and cultural integration. The ECSP has focused on cultural, medical and wellness tourism, which will further sustainable tourism opportunities between the two countries.

The flourishing tourism sector has also acted as a catalyst for trade. Low-cost airlines such as Vietjet and IndiGo have rapidly expanded their networks, directly boosting air travel and accelerating investments in hospitality by Indian and Vietnamese conglomerates. Beyond holiday getaways, Vietnam has also emerged as a major hub for meetings, exhibitions and Indian destination weddings. This has led to an influx of Indian tourists, fostering social and cultural familiarity and adaptation. The hospitality sector in Vietnam, including hotels and local tour operators, has adapted by training staff in Indian cultural preferences and opening authentic Indian restaurants, thereby attempting to bridge the cultural gap.

Social media platforms and their feeds have amplified travellers’ wish lists for destinations such as beaches in Da Nang and Phu Quoc, heritage cities like Hoi An and Hue, and the urban landscapes of Hanoi and Ho Chi Minh City. This has shifted Indians’ perception of Vietnam from a historically war-torn country to a vibrant, culturally rich, and affordable luxury destination, an alternative to expensive European holiday destinations.

Given the deep civilisational linkages between India and Vietnam, the two countries have agreed to collaborate on digitising ancient Cham manuscripts and to promote research into their shared civilisational and Buddhist heritage. Committed to deepening academic ties and institutional research, both countries have agreed to enhance educational cooperation and academic exchanges between their institutions. This expansion of people-to-people exchanges has been a major pillar of political cooperation between the two countries, leading to growing trust and a strong public mandate for enhanced diplomatic alignment.

Conclusion

The India-Vietnam ‘Enhanced Comprehensive Strategic Partnership’ is forward-looking. It is a highly ambitious framework rooted in civilisational ties and shared geopolitical interests. Bilateral relations are underpinned by mutual interdependence in a rapidly shifting geopolitical order. Both countries firmly support a ‘free, open and rules-based’ Indo-Pacific. They share security interests to counterbalance regional security concerns and oppose any coercion by any hegemonic power.

Vietnam remains a vital anchor of India’s Act East policy. The partnership has been strengthened by Vietnam’s accession to the IPOI, which aligns with Vietnam’s regional perspective. Under ECSP, the institutionalisation of the 2+2 Defence Dialogue further reinforces the commitment to a ‘rules-based’ security architecture in the region. On the economic front, both countries have set a high bilateral trade target of USD 25 billion by 2030. They are also diversifying supply chains and strengthening digital ecosystems through strategic MOUs covering critical minerals, digital connectivity, urban governance, and fintech. Overall, this partnership serves as a model for Indo-Pacific stability, underpinned by mutual trust and confidence, ensuring economic resilience and security in the maritime domain.

To conclude, it is worth quoting from Prime Minister Modi’s speech, which draws on Lord Buddha’s teaching, “If you light a lamp for someone else, it also illuminates your own path.” Reinforcing this principle, he adds, “By supporting each other’s visions and goals, we will collectively realise our aspirations to become developed nations.”

Author Brief Bio: Prof. Sonu Trivedi is a Distinguished Fellow at the India Foundation. She is also a Professor of Political Science at Zakir Husain Delhi College, University of Delhi.

REFERENCES

[1] Trivedi, Sonu. (2025). India-Champa: Shared Cultural Heritage in Southeast Asia, Vietnam Social Sciences Review, No. 2. pp. 26-37.

[2] Chakraborti, T. (2008). Strategic convergence between India and Vietnam in the twenty-first century: “Look East” as a parameter. Indian Foreign Affairs Journal, 3(4), 39–54.

[3] Trivedi, Sonu. (2025) Legacy of President Ho Chi Minh and India-Vietnam Relations. Vietnam Journal of Asian–African Studies. Volume 1, Issue 1, pp. 25-36.

[4] Embassy of India, Hanoi (2025). Bilateral Relations, URL: https://www.indembassyhanoi.gov.in/page/bilateral-relations/

[5] Hindustan Times (2026, May 6). India, Vietnam elevate ties, conclude 13 agreements across sectors. URL: https://www.hindustantimes.com/india-news/india-vietnam-elevate-ties-conclude-13-agreements-across-sectors-101778089308070.html

[6] DD News (2026, May 6). India, Vietnam elevate ties; PM Modi highlights trade growth, connectivity and strategic cooperation. URL: https://ddnews.gov.in/en/india-vietnam-elevate-ties-pm-modi-highlights-trade-growth-connectivity-and-strategic-cooperation/

[7] Ministry of External Affairs, India. (2026).

[8] Embassy of India, Hanoi (2026). List of Outcomes: State Visit of President of the Socialist Republic of Vietnam to India. URL: https://www.indembassyhanoi.gov.in/page/list-of-outcomes-state-visit-of-president-of-the-socialist-republic-of-vietnam-to-india-may-05-07-2026/

[9] Ministry of External Affairs, India. (2026).

[10] Ministry of External Affairs, India. (2026).

[11] Ministry of External Affairs, India. (2026).

[12] Ministry of External Affairs, India. (2026).

[13] Ministry of External Affairs, India. (2026).

[14] Ministry of External Affairs, India. (2026).

[15] Narendra Modi. (2026, May 6). English Translation of Prime Minister’s Press Statement during the Joint Press Statement with the General Secretary of the Communist Party of Vietnam and the President of Vietnam. URL: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2258346®=3&lang=2

[16] EXIM Bank (2020). India Securing Rare Earth Elements. Working Paper No. 97. URL: https://www.eximbankindia.in/sites/default/files/2025-07/132file.pdf

[17] Vinfast (2024). Vietnam’s VinFast breaks ground for ₹4,000 crore EV factory in Tamil Nadu. URL: https://vinfastauto.in/en/press-release/vietnams-vinfast-breaks-ground-for-rs4000-crore-ev-factory-in-tamil-nadu

[18] The Telegraph (2026, May 22). Vietnam’s big electric car bet on India with plans for thousands of cabs. URL: https://www.telegraphindia.com/business/vietnams-big-electric-car-bet-on-india-with-plans-for-thousands-of-cabs/cid/2161794#goog_rewarded

From Vulnerability to Resilience: Redefining India’s National Maritime Energy Security Doctrine

The Indian Ocean Region (IOR) remains of immense importance to India, as it carries 40% of global commercial trade traffic and almost 70% of the world’s energy trade. India has a significant presence in the region, given its peninsular geography, which extends deep into the Indian Ocean, with the Arabian Sea and Bay of Bengal on its western and eastern sides, respectively. India, with its fast-growing economy and efforts to become a global manufacturing hub, will need to secure the maritime routes available to it for commercial trade.

Consequently, securing maritime security in the area is urgent, as these Sea Lines of Communication (SLOCs) are the main arteries for sustaining and advancing its national growth plans, securing National Security, and maintaining its influence in the region. The target of becoming a developed nation by 2047 under the ‘Viksit Bharat’ can only be achieved by adopting a multipronged strategy that ensures the continued availability of maritime routes and a credible naval presence along them, thereby mitigating any potential threat to our national interests. It is important to recognise that 95% of India’s trade and more than 90% of India’s energy imports depend on this maritime connectivity.

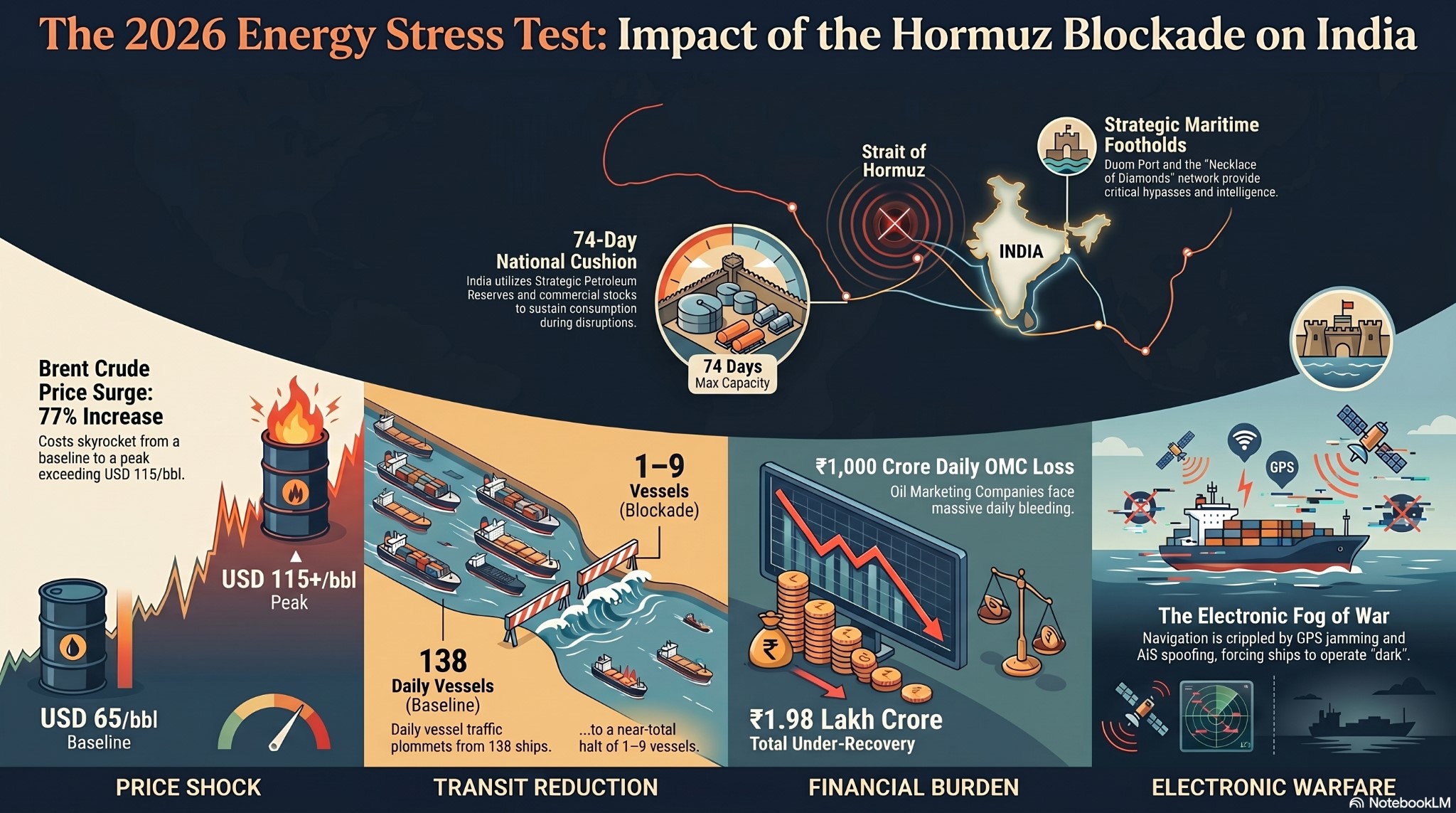

For decades, a global consensus held that vital maritime trade routes would not be disrupted given the catastrophic economic shocks such an action would trigger. That assumption was shattered in February 2026. The outbreak of the Israel-US conflict with Iran led to the complete closure of the Strait of Hormuz to international shipping, sending shockwaves through global energy security—with India particularly vulnerable. Consequently, global crude prices surged from a pre-war benchmark of USD 65 per barrel to a staggering USD 115 per barrel.

This has had a far-reaching impact on India and driven home a harsh lesson: India’s energy security can no longer be managed through long-term contracts. Instead, India needs a multi-pronged strategy to mitigate risks by immediately expanding strategic reserves, addressing critical chokepoint vulnerabilities through an effective countermeasure policy, and mitigating navigational challenges, including GPS disruptions and AIS spoofing for shipping vessels. India must have its own infrastructure to capture maritime awareness, strategic bilateral and multilateral partnerships with friendly energy-sourcing countries, and formidable naval influence covering this most important sea line of communications.

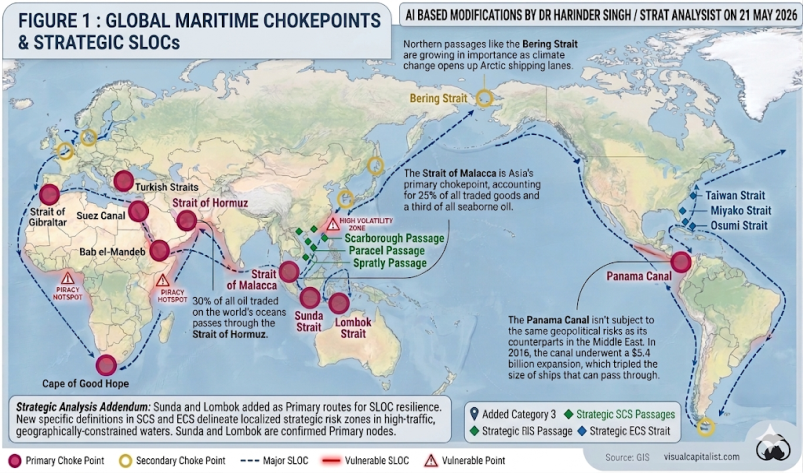

The Operational Layer: Anatomy of Chokepoints and SLOCs

There are four maritime routes or corridors that affect India’s energy security. Each presents both common and distinct physical, geopolitical and operational challenges. Of these, the Strait of Hormuz is the most critical chokepoint for India’s energy imports, as historically nearly 80% of Indian crude oil imports and nearly 60% of LPG needs have used this route. It is an exceptionally narrow sea route, only about 3 km wide, that is navigable by crude oil tankers and LPG vessels. The route is said to have a capacity to handle 20 million barrels per day. About 130-140 ships used to cross this narrow sea lane in the pre-war period, which has reduced to a single-digit figure post 28 Feb 2026 war. This has severely affected the movement of India-bound tankers and vessels. The effect has led India to seek alternative sources of crude oil beyond the Middle East, resulting in critical delays, increased freight rates, and higher insurance premiums. All this has resulted in a substantial increase in Indian bucket prices, which reached a peak of USD 140 per barrel, according to some reliable sources. Any prolonged escalation of these geopolitical situations will put immense pressure on India, seriously affecting its GDP growth. India has now increased the number of countries it sources crude oil from from 27 to 47 and has also raised domestic LPG production by more than 40%.

The Strait of Malacca is India’s eastern vulnerability. It handles 16 million barrels of crude oil per day and is the only maritime route connecting to energy sources in the Pacific Ocean. Nearly 60% of India’s commercial trade uses this route, and 100% of non-Gulf LNG trade passes through this vital chokepoint. Any disruption of this route will severely jeopardise India’s interests; if there is any simultaneous blockage of the western Hormuz route and the Strait of Malacca, it will be catastrophic for India. Effective maritime security is an urgent requirement for India to maintain continuity of trade via the Pacific Ocean LNG route and other commercial trade with East Asian countries.

The Bab el-Mandeb Strait and the Suez Canal collectively serve as the gateway to Europe and North Africa. Any disruption on this route, whether through drone attacks, missile batteries, or high-speed armed boats originating from coastal belt areas in this region, will seriously disrupt vessel traffic. If such asymmetrical warfare methods are used, they will force traffic to be rerouted around the African continent via the Cape of Good Hope. This will add 3,500 nautical miles, cause a 10-14-day delay, and incur exorbitant freight and insurance premiums, which will be highly detrimental to trade and the broader economic context of our country.

Tactical disruptions via GPS denial and electronic warfare severely impair the efficient navigation of ships along routes in this area. There have been reports of heavy GPS jamming and AIS spoofing in the Arabian Sea, the Gulf of Oman, and the high seas adjoining Fujairah. These tactical disruptions have led to errors in the navigation system and corrupted navigation. This is a serious issue that increases the risk of collisions and accidents involving shipping vessels. Another threat is the potential exposure of exact positions to asymmetric warfare by terrorists and rogue sea elements, which has often forced civilian ships to switch off their AIS transponders to avoid potential attacks. Therefore, for India, it has become an unavoidable requirement to preserve navigational integrity and maritime awareness by deploying its own infrastructure, including the ISRO-developed NavIC satellite navigation system, and by equipping its naval and commercial ships with these technologies. The absence of these measures will surely render our military and commercial assets in navigational darkness.

The February 2026 crisis emerging from the Israel-America-Iran war has further exposed vulnerabilities stemming from digital platforms’ weaknesses against cyberattacks, space-based weapons, and unmanned platforms powered by Artificial Intelligence (AI). This war has demonstrated how these technologies were extensively employed by America and Israel to completely destroy or deny Iranian naval resources the ability to even respond to their first attack. All the air defence infrastructure, be it on the ground or on board Iranian naval platforms, was rendered useless or completely destroyed by combining conventional airpower and naval platforms with these third-dimensional force multipliers.

These vulnerabilities are strategically significant because nearly 95% of global digital communications traffic is transmitted through submarine cable networks, many of which traverse the Indian Ocean Region. Simultaneously, the proliferation of autonomous drones, loitering munitions and low-cost precision-strike systems has reduced the barriers to asymmetric maritime disruption, enabling even non-state actors to threaten offshore energy infrastructure and commercial shipping lanes. This evolving operational environment requires us to move beyond conventional naval preparedness toward integrated maritime-electromagnetic resilience. Energy security in the coming decades will depend not only upon naval presence but also upon digital survivability, cyber resilience and uninterrupted access to secure maritime data networks. Accordingly, India’s future maritime-security architecture must incorporate anti-jamming navigation capability, indigenous satellite redundancy, AI-enabled maritime-domain awareness, cyber-secure port infrastructure and integrated civil-military digital coordination mechanisms.

Note: The above Infographic is original work generated using Google NotebookLM AI.

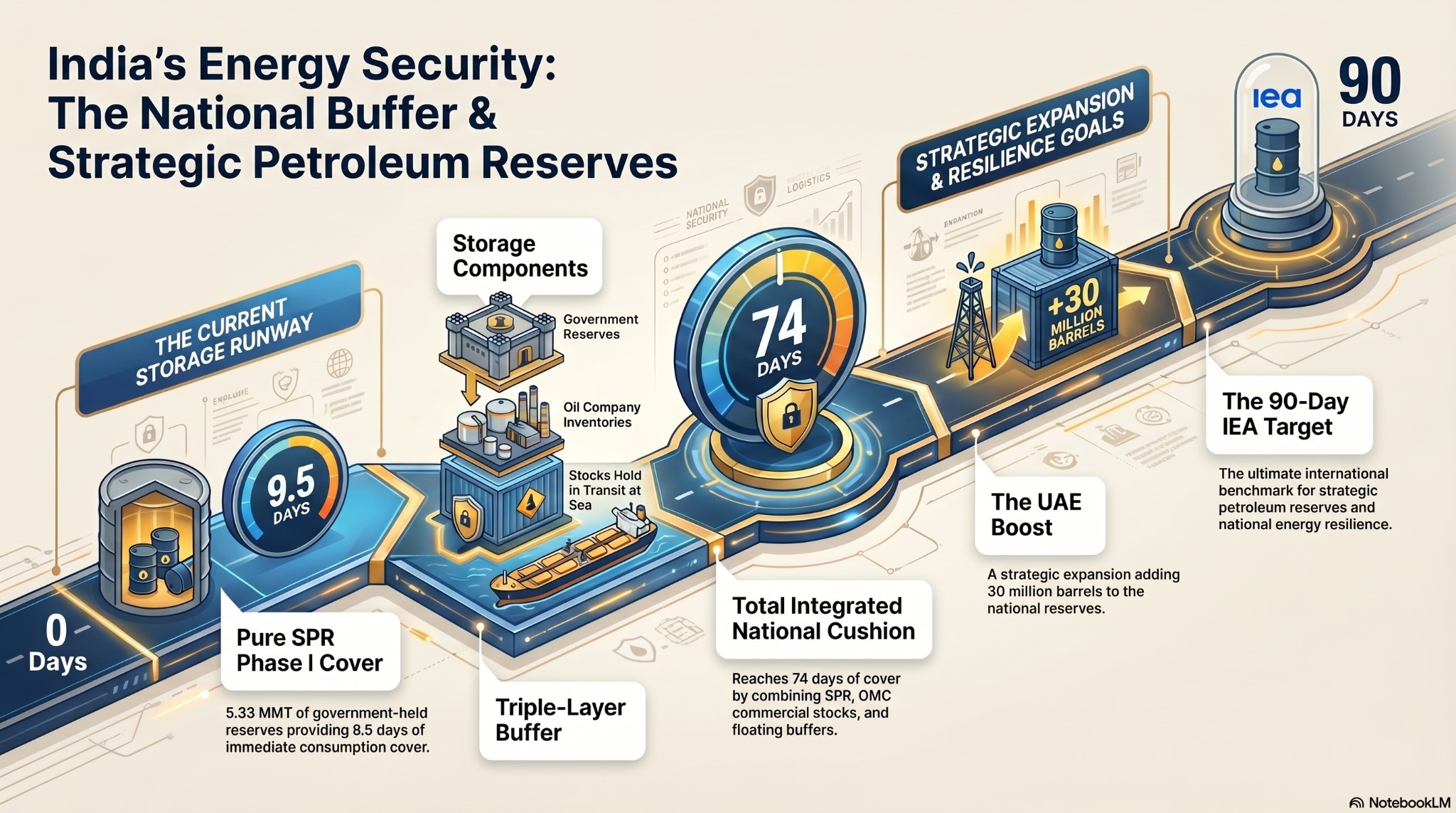

The Economic Buffer: India’s Strategic Reserves

In response to the severe operational and economic disruptions triggered by the 2026 crisis, India was forced to adopt major changes to its energy-security strategy. The shift reflected a broader strategic realisation that energy security depends not on procurement contracts but on effective control over logistics infrastructure, storage capacity, maritime access to routes, and supply-chain continuity. This change led to the event that during the Prime Minister’s May 2026 visit to Abu Dhabi, a series of strategic agreements were envisioned between India and the UAE.

The Strategic Petroleum Reserve was conceptualised on 16 Jun 2004. It has remained the backbone since then, with implementation carried out in phases. A further development, the adoption of out-of-the-box solutions, has emerged recently, including bilateral and multilateral agreements with friendly sourcing countries. The following are the main implementation frameworks that have emerged so far:

Phase-I Status

SPR Phase-I provides a storage capacity of 5.33 Million Metric Tonnes (MMT) which is equivalent to approximately 9.5 days of national consumption. The reserve infrastructure is distributed across three underground unlined rock cavern sites:

- Visakhapatnam (AP): 1.33 MMT

- Mangaluru (Karnataka): 1.50 MMT

- Padur (Karnataka): 2.50 MMT

In addition, India depends on the rolling inventories of the Oil Marketing Companies (OMCs) such as IOCL, BPCL, and HPCL, which include their own static storage and mobile transportation assets, amounting to 64.5 days’ worth of consumption stock. Of this total, refineries hold half in crude oil and the other half in finished products such as petrol and diesel. The total aggregated storage in these wats amounts to 74 days’ reserves. For LPG, India is completely dependent on OMC rolling inventory, amounting to 45 days of consumption and 60 days’ worth of LNG.

Phase II Expansion

Phase II received ‘in-principle’ Cabinet approval in June 2018 and financial approval under the PPP model in July 2021. However, progress was delayed due to a scarcity of funds and issues with land acquisition for the project. It is reliably learnt that, in the aftermath of the ongoing geopolitical disruptions in the Middle East, the Government has now fast-tracked the project. The SPR Phase II expansion remains critical for long-term resilience. Once fully operational, India’s standalone strategic cover could expand to approximately 22 days. The approved expansion includes:

- Chandikhol (Orissa) : 4.0 MMT

- Padur Expansion (Karnataka): 2.5 MMT

- India-UAE Strategic Reserve Framework.

In a new development, a series of strategic agreements were envisioned between India and the UAE. This arrangement could significantly increase India’s capacity for autonomous energy security insulation. Under the proposed India-UAE strategic partnership framework, ADNOC could commit approximately USD 5 billion towards infrastructure, technology and strategic storage investments. India could secure the ability to store up to 30 million barrels of crude oil within Indian reserve facilities. India could retain sovereign first-use rights during emergency conditions.

Note: The above Infographic is original work generated using NotebookLM AI.

SPR Phase I Cover: 5.33 MMT (9.5 Days).

Total Integrated Cushion: 74 Days (SPR + OMC commercial stocks).

The UAE Boost: 30-million-barrel addition to meet the 90-day IEA international goal.

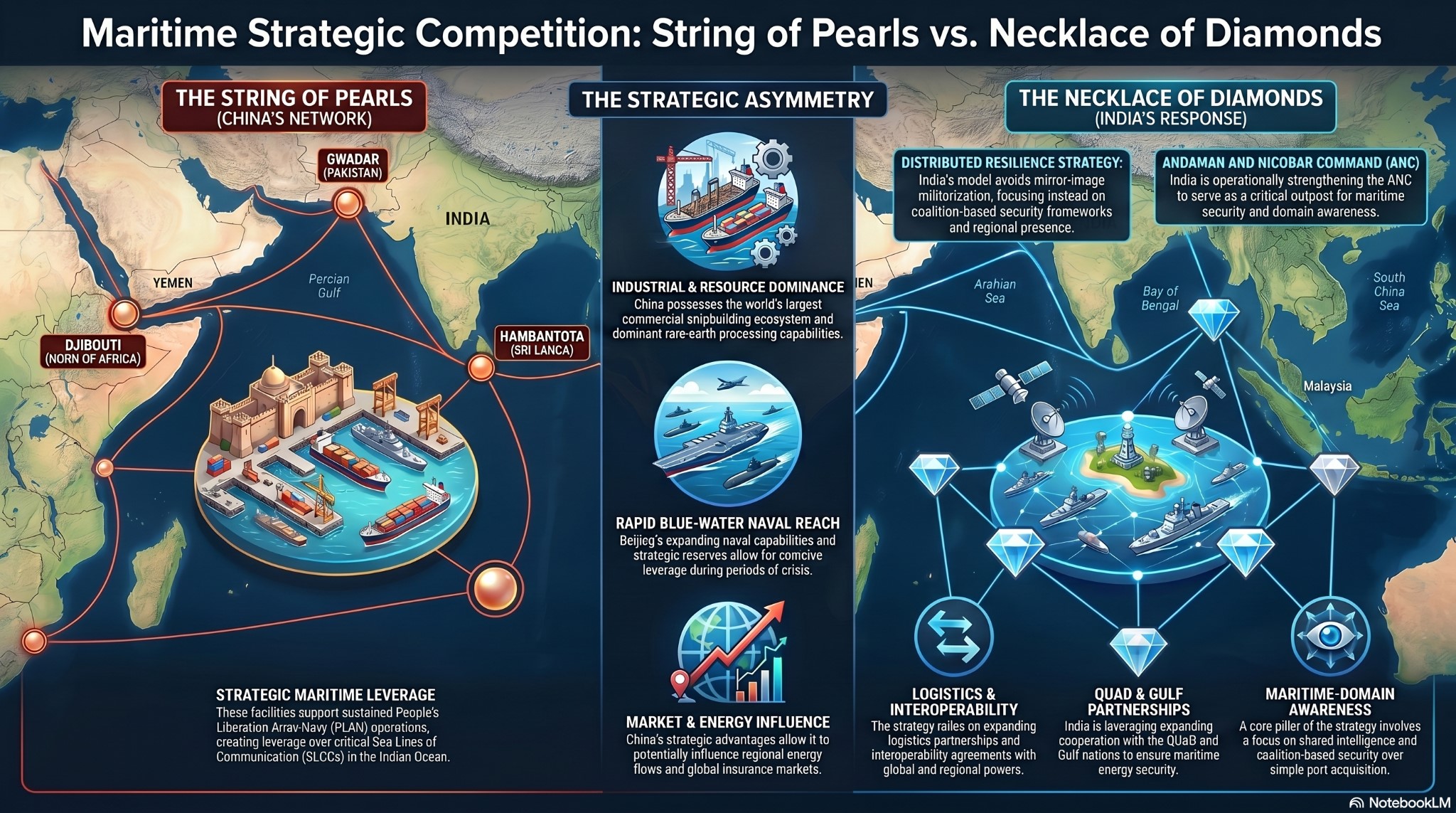

The Strategic Layer: “The String of Pearls” Vs “Necklace of Diamonds”

India’s maritime energy strategy cannot be understood in isolation from China’s expanding strategic footprint across the Indian Ocean Region (IOR). Over the past decades, China, with some seemingly not-so-good intentions, has developed a network of dual-use ports, logistics nodes and infrastructure partnerships popularly known as the ‘String of Pearls’. While officially presented as commercial infrastructure under the Belt and Road Initiative (BRI), several of these facilities possess military capabilities for supporting People’s Liberation Army Navy (PLAN) operations across the Indian Ocean.

Chinese increased presence at Gwadar (Pakistan), Djibouti (Horn of Africa), Hambantota (Sri Lanka) and growing access in the Gulf region collectively create the possibility of maritime influence over the Sea Lines of Communication (SLOCs). This becomes particularly significant because India’s energy security architecture remains heavily dependent upon uninterrupted access to the Gulf.

Note: The above Infographic is original work generated using NotebookLM AI.

The challenge for India is not only a conventional Naval competition but the risk of an asymmetry. China possesses the world’s largest commercial shipbuilding ecosystem, extensive rare-earth processing capabilities, large strategic reserves, and a rapidly expanding naval reach. During periods of crisis, these advantages may translate into substantial maritime advantages, leading to influence over regional energy trade.

India’s response, through its ‘Necklace of Diamonds’ strategy, aims to establish a distributed presence rather than pure militarisation. Unlike China’s port acquisition model, India’s approach emphasises logistics partnerships, bilateral and multilateral agreements, maritime awareness, and coalition-based security arrangements. The operational strengthening of the Andaman and Nicobar Command, together with the expansion of QUAD cooperation and Gulf partnerships, reflects India’s recognition that maritime energy security will increasingly depend on regional presence, distributed logistics capabilities, and partnerships. The Andaman and Nicobar Command, located approximately 100 nautical miles from the western entrance to the Strait of Malacca, serves as a forward operating platform for maritime awareness, surveillance, logistics support, and sea-lane monitoring. INS Baaz and related infrastructure projects will significantly strengthen India’s eastern maritime presence.

To counter China’s strategic encirclement by securing access to countries surrounding India under the guise of economic and commercial partnerships, India is working to establish a counter-presence in friendly neighbouring countries to create ship repair facilities, logistics centres, and maritime awareness coalitions within a legitimate security framework. India has been developing maritime repair facilities at Vadinar in Gujarat. The facility is being developed in collaboration with Drydocks World, a DP World company, and Cochin Shipyard Limited, and in partnership with the Deen Dayal Port Authority, to create a large ship repair cluster that will also cater for repairs to naval vessels. This is in line with the Indian Government’s Maritime India Vision 2030 and Maritime Amrit Kaal Vision 2047.

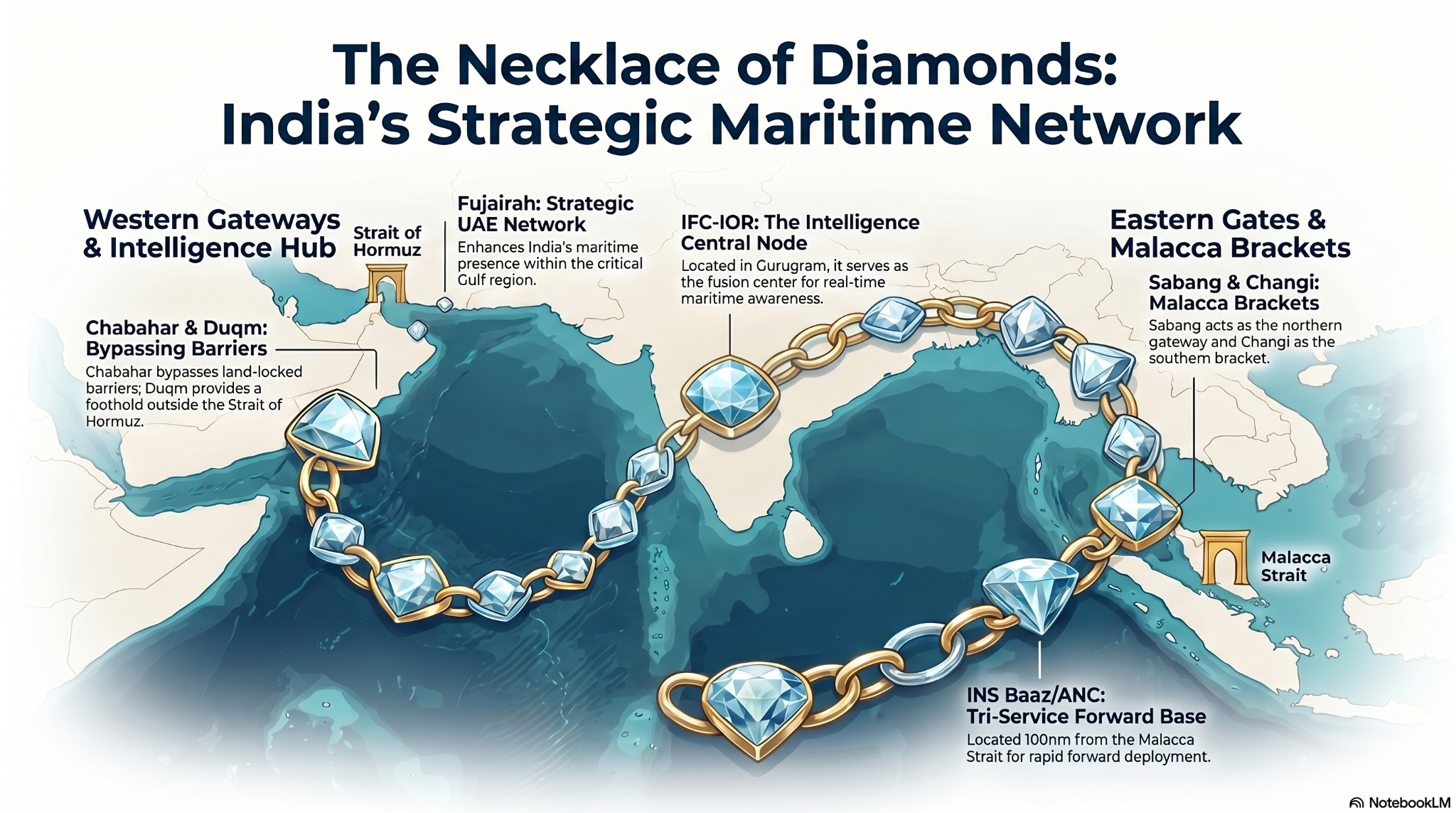

Apart from this, India is focused on getting access to the following strategic nodes outside the mainland:

- Fujairah, UAE. It is one of the most strategically located nodes in the Indo-Gulf region, which provides a bypass of the Strait of Hormuz. It also provides an alternative overseas strategic storage capacity, largely immune to disruptions at the mouth of the Strait of Hormuz or in the Persian Sea.

- Duqm Port, Oman. Duqm, due to its location away from Hormuz, can again serve as a Naval refuelling hub and provide ship repair facilities.

- Chabahar Port, Iran. Despite Iran’s instability, Chabahar remains a strategically critical Indian maritime asset, to which India has invested USD 120 million, fully paid in August 2025. The investment has been made to develop the Shahid Beheshti terminal. The port provides access to Central Asia, bypass capability around land barriers, geopolitical presence within Iran, and connectivity to INSTC corridors. The investment remains linked to the International North–South Transport Corridor (INSTC), with a 750 km Chabahar–Zahedan railway line linking the port directly to Central Asia and Russia, preserving the long-term commercial intent of India’s trade bypass around Pakistan.

- Sabang Port, Indonesia. Sabang provides India with a forward eastern maritime presence near the Malacca Strait. The location strengthens bilateral patrol coordination, anti-piracy operations, and regional surveillance capability.

- Changi Naval Base, Singapore. India has inked logistics agreements with Singapore to facilitate the sustained operational presence of Indian naval assets near the southern end of the Strait of Malacca. This effectively extends India’s operational reach into the Pacific.

Physical assets and maritime deployments alone cannot secure the interests of stakeholders in the Indian Ocean. India’s maritime doctrine has therefore evolved from SAGAR (Security and Growth for All in the Region), launched in 2015, to MAHASAGAR (Mutual and Holistic Advancement for Security Across the Region), launched in March 2025. Through this endeavour, India seeks to have the world recognise that it is now willing to contribute as a global maritime stakeholder, transitioning from a regional security provider to its friendly nations.

Note: The above Infographic is original work generated using NotebookLM AI.

Conclusion and Strategic Recommendations

The 2026 maritime crucible (Middle East War) marks a major turning point for India and the broader Indo-Pacific stakeholders. The crisis that erupted has shown that maritime chokepoints can severely disrupt both large and small nations without mercy. Weaker economies, or those that have not developed resilience in their energy security, can be severely damaged or even destroyed. Therefore, it is important to build and maintain strategic reserves of crude oil and LNG/LPG, ensure credible naval access to secure maritime routes, and deploy technological measures to counter cyber-attacks, GPS jamming, EW, and digital security threats. This is an urgent requirement to safeguard national interests, absorb such shocks, and protect the country’s economic growth. It is equally important to pursue international collaborations to mitigate the risks of any misadventures along or in the maritime trade routes. There is an immediate requirement for India to redefine its maritime security to ensure energy security and protect its broader macroeconomic interests.

Strategic Energy Resilience. India must accelerate the expansion of Strategic Petroleum Reserve (SPR) infrastructure by rapidly operationalising the Chandikhol site, the Padur expansion, and the Rajasthan salt-cavern ecosystems. Rapid-access storage architecture is most important during future maritime disruptions and energy shocks. Simultaneously, India requires dedicated underground LNG and LPG reserve systems capable of providing at least 30 days of independent strategic insulation. Gas security is now closely linked to fertilizer production and to energy availability for rural and urban consumption. It is also linked to transport networks and power generation.

Maritime and Digital Security Architecture. The crisis also demonstrated that navigational independence and maritime awareness are core national security requirements. India must therefore accelerate the deployment of NavIC-based maritime navigation systems, anti-jamming capabilities, AIS redundancy frameworks, and resilient maritime electromagnetic infrastructure. India’s future maritime security must also prioritise indigenous Intelligence, Surveillance and Reconnaissance (ISR) capabilities, integrated with space-based systems. Undersea communication cables must likewise be recognised as critical infrastructure because of their role in global financial systems, digital commerce, and military communications.

Indo-Pacific Strategic Coordination. India’s maritime security strategy must increasingly operate through regional partnerships and distributed resilience frameworks. Institutions such as IORA, BIMSTEC and the QUAD provide the foundation for a coordinated Indo-Pacific maritime security architecture focused on SLOC continuity, crisis coordination, dark-target identification and chokepoint resilience. Strategic infrastructure partnerships with the UAE, Oman, Singapore, Indonesia and Iran should evolve into long-term maritime resilience ecosystems that support logistics continuity, operational persistence and emergency energy access during periods of regional instability. Simultaneously, the QUAD framework offers substantial potential for coordinated maritime domain awareness, logistics interoperability and Indo-Pacific energy security cooperation.

Towards a National Maritime Energy Security Doctrine. A formal National Maritime Energy Security Doctrine would help institutionalise inter-ministerial coordination and align long-term strategic planning across operational, economic and technological domains. Such a doctrine would provide the foundation for India to transition from a vulnerable maritime energy consumer to a resilient Indo-Pacific maritime power. The 2026 crisis demonstrated that India’s future energy security can no longer be managed through fragmented institutional mechanisms operating independently across the defence, shipping, petroleum and digital infrastructure sectors. India presently lacks a unified doctrinal framework that integrates naval operations, strategic reserves, maritime infrastructure, cyber resilience, energy logistics and economic continuity planning.

For India, the future of energy security increasingly depends on ownership of energy resources and the ability to secure maritime access to them across contested oceanic trade routes. India’s energy security architecture needs to be shaped not only by procurement contracts but also by logistics resilience, chokepoint-bypass capability, maritime awareness, technological sovereignty, and strategic partnerships. The 2026 crisis demonstrated that maritime geography remains the ultimate determinant of energy continuity in an interconnected global economy. Future conflicts are likely to span physical, digital, electromagnetic and economic domains. This necessitates India developing integrated, dependable frameworks rather than conventional models. India’s evolving response is being shaped by strategic reserves, distributed maritime partnerships, digital platform maturity, naval modernisation and regional diplomacy. This marks a major transition from reactive dependence to a proactive approach. If India can sustain this through long-term institutional coordination and investment, this transformation could position India not merely as a major energy consumer but as a stabilising Indo-Pacific power. In the present and the future, energy security is no longer defined by possession of fuel reserves alone but by uninterrupted control over the maritime, digital and logistical systems that enable continuous energy availability.

Author Brief Bio: Wg Cdr Sanjay Kamra (Veteran) is an Electrical and Aeronautical Engineer, PMP-certified strategic advisor and former Indian Air Force officer with 30+ years of experience in defence communications, telecom infrastructure, RF systems, UAV ISR and strategic technology programmes. He advises defence, aerospace, telecom and emerging technology organizations on secure communications, critical infrastructure and government engagement.

Endnotes:

- Ministry of External Affairs, Government of India, “Prime Minister’s Visit to the United Arab Emirates (May 15, 2026),” May 15, 2026, https://www.mea.gov.in/press-releases.htm?dtl/41146/Prime+Ministers+visit+to+the+United+Arab+Emirates+May+15+2026.

- Press Information Bureau, Government of India, “Prime Minister’s Visit to the UAE,” May 15, 2026, https://www.pib.gov.in/PressReleasePage.aspx?PRID=2261611&lang=1®=3.

- Prime Minister’s Office, Government of India, “List of Outcomes: PM’s Visit to the UAE,” May 15, 2026, https://www.pmindia.gov.in/en/news_updates/list-of-outcomes-pms-visit-to-the-uae/.

- Prime Minister’s Office, Government of India, “List of Outcomes: Visit of His Highness Sheikh Mohamed bin Zayed Al Nahyan, President of UAE to India,” January 19, 2026, https://www.pmindia.gov.in/en/news_updates/list-of-outcomes-visit-of-his-highness-sheikh-mohamed-bin-zayed-al-nahyan-president-of-uae-to-india/.

- Petroleum Planning and Analysis Cell (PPAC), Ministry of Petroleum and Natural Gas, Government of India, Ready Reckoner: Oil and Gas Industry Information at a Glance, FY 2025–26 (New Delhi: PPAC, 2026).

- Indian Strategic Petroleum Reserves Limited (ISPRL), Strategic Petroleum Reserve Facilities: Technical and Operational Status Reports for Visakhapatnam, Mangaluru, Padur, and Chandikhol (New Delhi: ISPRL, 2026).

- “Strategic Reconfiguration of Indo-Gulf Energy and Security Relations: A Geopolitical Analysis of the May 2026 India-UAE Agreements,” research paper, 2026.

- Discovery Alert, “PM Modi UAE Visit: India-UAE Energy Partnership 2026,” 2026.

- Discovery IQ, “ADNOC India Energy Storage and LNG Agreements Explained 2026,” 2026.

- Abu Dhabi National Oil Company (ADNOC), “Strategic Collaboration Agreement between ADNOC and Indian Strategic Petroleum Reserves Limited,” May 2026.

- Abu Dhabi National Oil Company (ADNOC), “Strategic Collaboration Agreement between ADNOC and Indian Oil Corporation Limited on Crude Oil and LPG Supply,” May 2026.

- “India’s Strategic Petroleum Reserves to Get Boost from ADNOC,” S&P Global Commodity Insights, May 15, 2026.

- “UAE-India Energy Security Partnership Strengthened by New ADNOC Agreements,” Energy Connects, May 2026.

- “UAE, India Agree to Expand Energy Supply Partnership,” Rigzone, May 2026.

- “Energy to Defence, India, UAE Deepen Ties as PM Modi Calls for Open Hormuz,” The Indian Express, May 2026.

- “India-UAE Energy Agreement: This Emirati Strategy Has Power,” The Economic Times, May 2026.

- “India-UAE Oil Reserve Pact Raises Hopes for Chandikhol SPR Project,” The New Indian Express, May 2026.

- “India-UAE Trade Relations and the Strategic Value of Recent Agreements,” India Narrative, 2026.

- “India-UAE Energy Deal 2026: Strategic Crude Shield Explained,” Defencera, 2026.

- Ministry of External Affairs, Government of India, “List of Outcomes: Prime Minister’s Visit to the UAE (May 15, 2026),” May 15, 2026, https://www.mea.gov.in/bilateral-documents.htm?dtl/41145/List_of_Outcomes_Prime_Ministers_Visit_to_the_UAE_May_15_2026.

- Reuters, “India Deepens Defence, Energy Ties with UAE during PM Modi Visit,” May 15, 2026, https://www.reuters.com/world/india/india-signs-pacts-with-uae-defence-petroleum-during-modis-visit-2026-05-15/.

- “PM Modi in UAE: India Signs Defence, Gas Supply and Strategic Oil Reserves Pacts with Abu Dhabi,” The Economic Times, May 15, 2026.

- “Short Trip, Big Results: Seven Crucial Deals Inked by PM Modi in UAE,” The Times of India, May 15, 2026.

Maritime Security, SLOC Vulnerabilities And India’s Maritime Goodwill Curve

Introduction: Chokepoint Paradox and multiplex Geopolitics

Strategic debates in India view national sovereignty in terms of territorial boundaries and continental security concerns. Yet, recent crisis around the Strait of Hormuz demonstrates that ‘India’s economic stability is equally dependent upon secure maritime trade corridors and resilient diplomatic partnerships requiring continuous regional cooperation.[1]’

As the world’s third-largest energy consumer, India’s economic growth remains heavily dependent on vulnerable maritime trade routes, creating what may be termed the “Chokepoint Paradox.” Historically, as Angus Maddison (2006) observed, India and China dominated global wealth through expansive trade networks[2].

Modern supply chains operate through dispersed production hubs and maritime transit networks. Under the present ‘Multiplex World Order[3]’, sea lane stability is no longer guaranteed by a single naval power. As Kishore Mahbubani’s “Great Convergence[4] suggest maritime stability increasingly depends upon cooperative management of shared space.

Yet contemporary policy remains hindered by ‘sea blindness’, prioritising land borders while underestimating the maritime foundations of national security.[5] Major chokepoints such as the Strait of Hormuz, the Strait of Malacca, and the Bab el-Mandeb remain vital corridors of global energy trade. They remain vulnerable to weaponised interdependence[6] of global economic and supply networks. Any constriction here rapidly affects freight costs, energy prices, industrial supply chains and the uninterrupted flow of hydrocarbons.

For too long, India’s ‘Maritime Strategy’ has emphasised naval force projection and the use of naval capability to secure uninterrupted energy flows. This approach is insufficient under present maritime conditions. India must move beyond a purely military understanding of sea control[7] to a broader maritime security, energy-resilient, and regional cooperation framework – namely “Multidimensional Energy Sovereignty (MES) framework”. By combining strategic planning with diplomacy, the framework operationalises India’s Maritime Goodwill Curve (IMGC)[8] and will help our nation transition from a ‘reactive security provider’ to a ‘proactive role’ in shaping regional maritime stability.

Strategic Fragility: Limitations of Conventional Maritime Security

The present-day ‘maritime threat environment’ extends beyond the reach of traditional naval responses. It has evolved significantly from the period dominated by Somali piracy, a comparatively limited maritime threat, to a more complex phase of ‘Hybrid Maritime Conflict’. Current threats increasingly include low-cost loitering munitions, Unmanned Underwater Vehicles (UUVs), and autonomous drone swarms. ‘Grey-zone tactics exploit the ambiguous space between peacetime commerce and open conflict.’[9]

Vulnerabilities of Hub-and-Spoke Supply Model.

Modern maritime logistics primarily relies on the Hub-and-Spoke (H&S) model, in which multiple regional sourcing locations (spokes) feed into centralised transit hubs before passing through critical maritime passages.[10] Although efficient under stable commercial conditions, it creates major concentration risks when these primary hubs or chokepoints are contested. During periods of asymmetric conflict, the high volume in these corridors makes them a high-value strategic target.

Carrier Battle Group (CBG) vs. 300% Insurance Premium

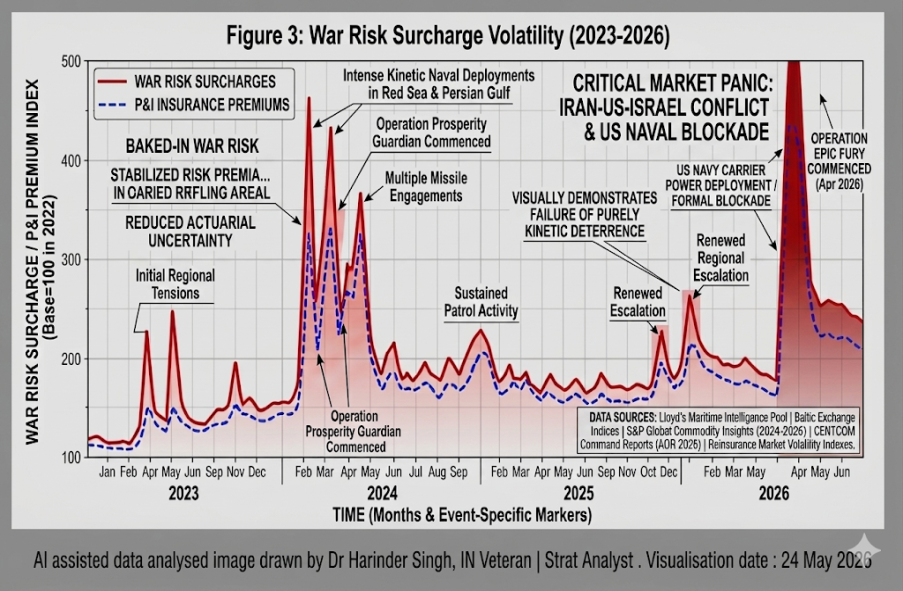

A Carrier Battle Group (CBG) alone cannot resolve prolonged maritime instability. Although it provides substantial deterrent capability, it also heightens concerns about regional escalation.[11] Transit premiums for vessels navigating contested chokepoints rise significantly during periods of instability, thereby substantially increasing commercial shipping costs. Analysis indicates that insurance premiums increased from the standard 0.07% of hull value to over 1.0%, resulting in a 300% to 500% increase in insurance costs.[12] Figure 3, ‘War Risk Surcharge Volatility’ diagram, placed here for the period 2023-2026, highlights the massive cost liabilities.

CBG or Naval deployments alone cannot fully resolve this insurance crisis due to three structural asymmetries:

- Cost-Exchange Asymmetry. We all understand that intercepting a ‘$20,000 Shahed-type drone with a $2.1 million SM-2 or $4.3 million SM-6 missile’[13] is operationally effective but financially unsustainable. Similarly, the insurance markets recognise the financial limits of such defensive responses during a prolonged crisis.

- Defensive Bubble vs. Dispersed Fleet. A CBG requires a substantial internal defensive screen to protect itself. It cannot provide point defence for individual merchant tankers scattered across a 500-mile transit corridor. Mandating convoys introduces ‘time-on-risk’ delays, increasing the actuarial probability of a mass-casualty event.

- Signal of Conflict. The arrival of a heavy naval task force acts as a force multiplier for market panic. It signals imminent kinetic escalation to reinsurance markets, permanently embedding “War Risk” clauses in maritime contracts.

Achilles’ Heel of Air-Sea Integration: Tanker Vulnerability & Incomplete AAR

The tactical limitations of carrier air elements are compounded by an operational bottleneck: India’s incomplete Air-to-Air Refuelling (AAR) capability and the fragility of support tankers in contested airspace.[14] Without persistent, long-range combat air patrols (CAP) over distant SLOCs, merchant vessels remain vulnerable to ballistic missiles and loitering munitions. Extending these air arcs requires a continuous AAR pipeline. However, the recent asymmetric downing of two large, non-stealthy refuellers highlights the catastrophic vulnerability of force-multiplier fleets.[15]

These lumbering, high-signature targets face immediate neutralisation. Their loss causes immediate fuel starvation for the forward-deployed fighter fleet, collapsing defensive air cover and leaving the naval task force and shipping exposed to saturation strikes. India’s current inventory of heavy refuellers (Il-78 MKI) is structurally limited in both volume and availability.[16] Attempting to patrol the Western Indian Ocean or the Bab-el-Mandeb with an incomplete, vulnerable AAR capability would invite operational paralysis. A Navy cannot command the surface if its aerial logistical spine can be severed by a single, low-cost munition. To secure sea lanes, India requires deep strategic goodwill in the littorals rather than mere naval firepower.

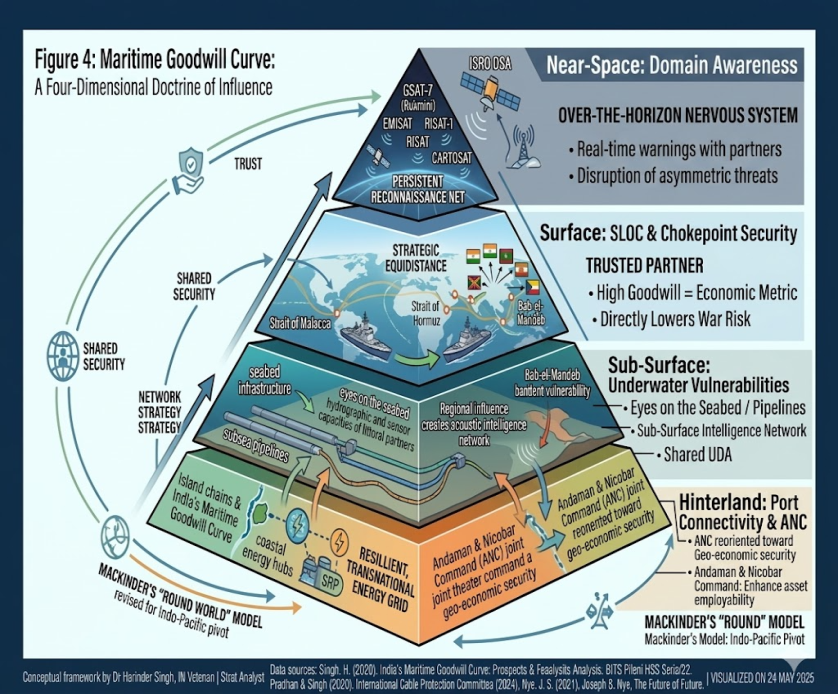

Maritime Goodwill Curve: Four-Dimensional Doctrine of Influence

To move beyond purely military responses, India needs to address the persistent trust deficit in key littoral regions bordering critical chokepoints. Classical geopolitical thinking, particularly Mackinder’s Heartland framework, “The Round World model”, revisited for the Indo-Pacific, reveals that controlling global sea lanes and island chains is an important geopolitical factor in the Indo-Pacific.[17]

To win and preserve regional peace, India’s Maritime Goodwill Curve (IMGC) framework offers a practical and more cooperative strategic approach.[18] It posits that energy transit security increasingly depends on the level of strategic trust with the littoral state.[19] Goodwill here is not merely symbolic diplomacy. It’s a measurable strategic asset. As Joseph Nye states, it’s a highly ‘Quantifiable Smart Power Asset’ with layered strategic advantage. Let us expand this doctrine within a four-dimensional operational framework to establish broader maritime resilience.

Near-Space: Space-Based Domain Awareness.

Modern maritime security is increasingly linked to space-based infrastructure. To deter asymmetric threats before they reach maritime chokepoints, we need to improve coordination between space and maritime surveillance systems. By integrating the capabilities of the Defence Space Agency (DSA) and ISRO, India can maintain continuous satellite-based maritime monitoring. This can be achieved by leveraging the CARTO, RISAT, and GSAT-7 (Rukmini) satellite series, along with the EMISAT electronic intelligence constellation. This space-to-sea linkage shall form an integrated early-warning network to support IMGC operations. By sharing satellite-derived, real-time early warnings with friendly regional partners, India can identify drone activity and piracy threats before they directly affect shipping lanes.

Sub-Surface: Underwater Vulnerabilities.

Subsea pipelines and communication cables form a critical part of global infrastructure. They are among the most vulnerable components of energy sovereignty. The surface fleet has limited ability to monitor sub-surface sabotage. This vulnerability of undersea communications cables was evident in Bab-el-Mandeb.[20] Rather than relying on continuous physical monitoring of the seabed, IMGC must operationalise shared Underwater Domain Awareness (UDA). By investing in the hydrographic and sensor capabilities of littoral partners, India can improve underwater monitoring capabilities while building a collaborative, regional, real-time underwater surveillance network.

Surface: SLOC & Chokepoint Security

This domain yields the most immediate ‘Goodwill Dividend’. At the surface tier, maritime sovereignty is maintained through Strategic Equidistance – using diplomatic agility to navigate a heavily sanctioned world as a trusted partner rather than a hegemonic threat. Regionally, high goodwill serves as an economic metric that directly lowers war-risk surcharges. When littoral states perceive India as a collaborative, non-threatening partner, operational friction and security premiums for Indian-flagged energy hulls decrease sharply.

Hinterland Tier: Port-to-Pillar Connectivity and ANC.

The maritime security continuum must extend inland to include critical infrastructure that receives, stores, and distributes imported energy. In the context of the Andaman & Nicobar Command (ANC), India’s island chains remain a paramount national asset.

As late as early 2015, the Cabinet Committee on Infrastructure Enhancement & Security in GoI was considering ways to enhance the employability of infrastructure and strategic assets in the A&N islands.[21] With the 2019 institutionalisation of the Chief of Defence Staff and our joint theatre command still in fieri, it’s time to reorient the latter towards India’s geo-economic security. This can be achieved by tethering our coastal energy hubs and Strategic Petroleum Reserves (SPR) to regional littoral networks. We can transform these domestic stockpiles into vital nodes within a resilient, transnational energy grid.

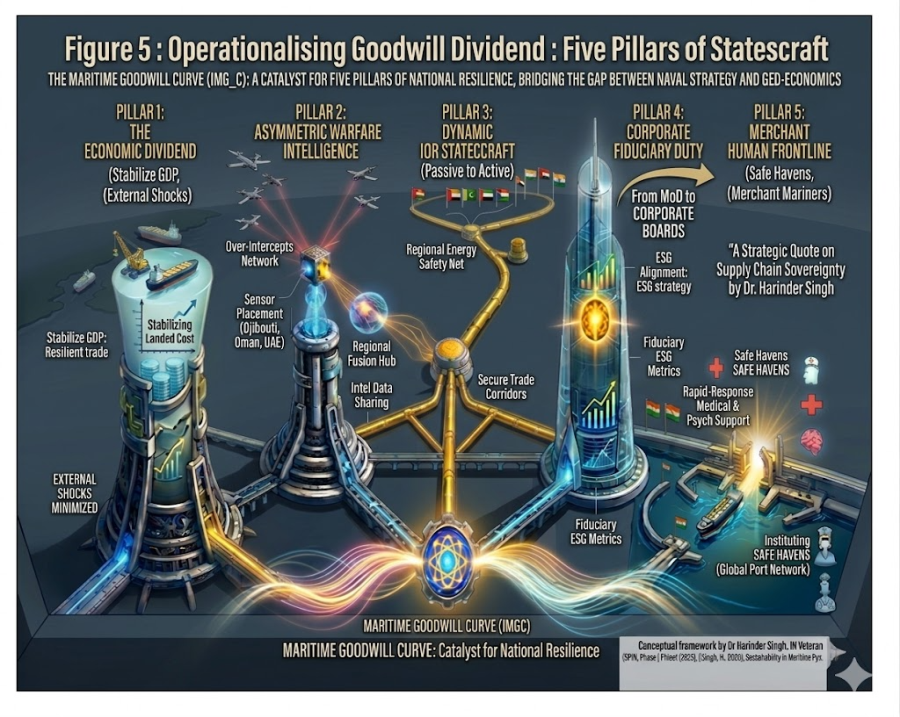

Operationalising Goodwill Dividend: Five Pillars of Statecraft

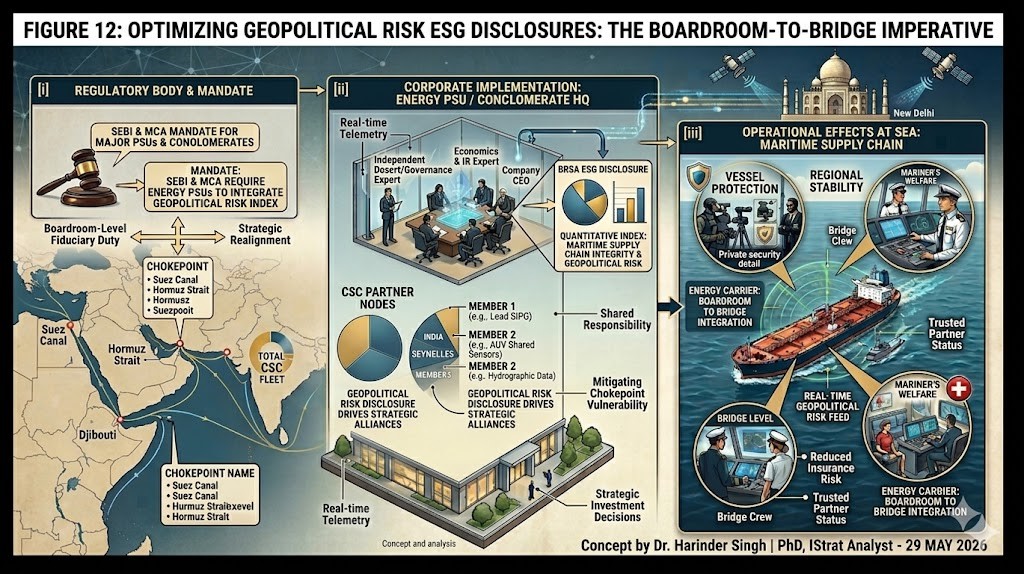

Maritime goodwill curve acts as a catalyst for five substantive pillars of national resilience, bridging the vital gap between naval strategy and geo-economics:-

Pillar 1: The Economic Dividend (Stabilising the Landed Cost). In the context of modern chokepoint volatility, the primary threat to India’s sovereignty is inflationary contagion from imported energy. When the Strait of Hormuz became contested, economic friction was evident in dramatically higher P&I insurance premiums. Unlike kinetic defence, which invites reciprocal aggression, the Goodwill Curve signals regional stability. By maintaining high-trust partnerships (through HADR, joint patrols, and capacity building), India actively reduces underwriters’ perceived risk, thereby protecting India’s GDP from external geopolitical shocks. This synergy between international diplomacy and maritime operations is critical to stabilising the maritime supply chain.[22]

Pillar 2: Asymmetric Counter-Warfare (Intelligence over Intercepts). Rather than attempting to ‘out-missile drone swarms’, the Goodwill Curve operationalises Regional Intelligence Fusion. High levels of strategic trust enable the forward placement of sensors and the seamless sharing of real-time intelligence with littoral partners (e.g., Oman, UAE, Djibouti). An early-warning data point shared by a friendly littoral neighbour is infinitely more valuable than a multi-million-dollar interceptor launched in isolation.

Pillar 3: Dynamic SPR Leadership (Regional Energy Safety Net). While India’s Phase II SPR expansion (adding a planned 4.0 Million Metric Tons (MMT) at Chandikhol and 2.5 MMT at Padur II under a commercial-cum-strategic Public-Private Partnership (PPP) model) is a critical domestic imperative,[23] the Goodwill Curve enables the Strategic Petroleum Reserves (SPR) to serve as a regional diplomatic asset. By positioning India as a regional energy guarantor, domestic stockpiles act as a stabilising force across the entire IOR. This transforms the SPR from a passive stockpile into an active tool of energy statecraft, ensuring our littoral partners are deeply invested in the safety of the sea lanes that supply our tanks.[24]

Pillar 4: Boardroom ESG Governance (Fiduciary Sovereignty). The mandate for national security must move swiftly from the Ministry of Defence (MoD) to the corporate boardrooms of India’s energy giants. We must reclassify maritime security as a core tenet of Environmental, Social, and Governance (ESG) strategy.[25]